There are several risk factors involved in making an investment, which can be significant if they materialise. Each risk may have a material effect on PDG's business, results of operations and financial condition and on the PDG's potential ability to achieve its financial objectives.

Risks related to investing include for example, but not limited to:

RISKS RELATED TO THE LEGAL STRUCTURE OF THE SECURITY OR INVESTMENT AND THE SECONDARY MARKET

Shareholders may lose all or part of their invested capital.

Shareholders of the company are equity investors and have no creditor position vis-à-vis the company in the event of insolvency. Shareholders may lose all or part of their invested capital. In the event of insolvency, shareholders only participate in the insolvency assets after the creditors have been satisfied.

The subscription price of the new shares may have been set too high.

The subscription price proposed by the Company is based on the Company's own estimates and was determined based on the enterprise value used for the last capital increase in the Company. The assumptions for the value of the company on which this assessment is based for the capital increases in the company could therefore be incorrect (in the absence of an enterprise value report) or prove to be incorrect in the future due to internal and external factors, so that the issuer's enterprise value would be set too high in this case.

There is no regulated secondary market for the shares and the shares are therefore not publicly tradable.

There is currently no organised secondary market for the issuer's shares. The decision as to whether the issuer's shares will in future be listed on a stock exchange, included in trading on a multilateral trading facility or another system is at the sole discretion of the issuer. Even if the shares are listed on a stock exchange or multilateral trading facility, there may be no significant active trading in the Company's shares. Currently, no listing of the shares on a stock exchange is planned. In addition, there is a risk that the determined value does not correspond to the calculated true value per share.

The value of the Company's shares may fluctuate significantly for other and completely different reasons, in particular as a result of fluctuating actual or forecast results, changed profit forecasts or the non-fulfilment of the profit expectations of securities analysts, changed general economic conditions or even in the event of the realisation of one or more risks.

In the event that the shares are not listed on a stock exchange in the future or are included in trading on a multilateral trading system, shareholders will not have the opportunity to sell the shares via the market and will have to look for other disposal options on their own. This can be time consuming and costly. In addition, there is then no reference price formed via the market at which transactions can be made with the shares. Any suspension or interruption of trading, in the case of public tradability of the shares, may also have a negative impact on the tradability of the Company's shares and thus on the price of the shares.

The transferability of the shares is limited and the pledging and/or other encumbrance requires approval.

The shares may only be transferred to natural or legal persons who have joined the Minority Shareholder Agreement of the issuer valid at the time of the transfer. In accordance with the Minority Sharhoder Agreement, the pledging and/or other encumbrance of the shares requires the approval of the issuer in the form of a Management Board resolution. There is therefore the risk of not being able to sell the shares without the consent of the Management Board, remaining a shareholder of the issuer and thus not being able to generate any proceeds from the sale.

Any future capital increases of the Company may dilute the share of existing shareholders in the Company's share capital and affect the price of the shares.

Should a capital increase of the company be carried out without granting or exercising subscription rights by the shareholders, this may lead to a dilution of the shareholders' shares. Such capital increases may affect the value of the shares and, in the event of an exclusion of subscription rights, dilute the share of existing shareholders in the Company's share capital.

Obligations of shareholders in the event of exit may lead to an obligation to carry the shares.

Under the terms of the Minority Shareholder Agreement, in the event of a transfer of all or substantially all of the shares, a sale of all or substantially all of the Company's assets, a merger, restructuring or other transaction in which all existing shareholders will hold less than 50% of the Company's shares after the Transaction or, in the event of the listing of the Issuer's shares in a recognized Exchange ("Exit") to take all necessary and appropriate actions to enable the implementation or completion of the exit. This obligation may also include the obligation to transfer the shares at a price not to be determined by the shareholder himself. In such a case, the shares of all shareholders are transferred on equal terms.

RISKS INHERENT IN SOCIETY OR ITS INDUSTRY

Entrepreneurial risk.

The shares are an entrepreneurial investment. The investor participates in the issuer's entrepreneurial business risk with his paid-in capital. Statements and assessments of future business development may be or become inaccurate. Economic success depends on many influencing factors, in particular the development of the respective market and circumstances that the issuer cannot or only partially influence.

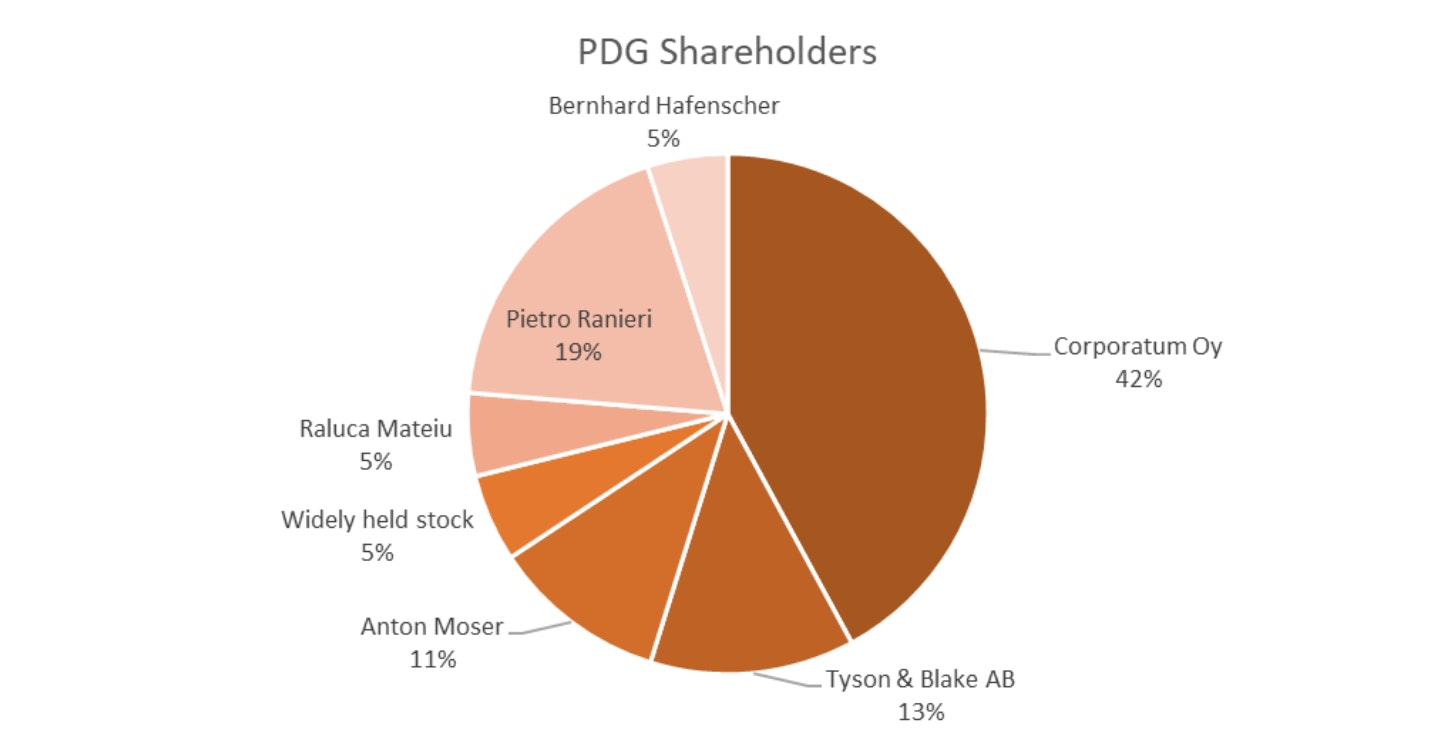

Risks relating to the Company and its shareholder structure.

The capital increase will be carried out by issuing up to 1,578,948 new shares (no-par value shares). The existing shareholders hold 10,000,000 no-par value shares. The voting rights of shareholders depend on the number of no-par value shares. Accordingly, one vote per share is due. The issuer's dividend policy provides for no distributions to shareholders at least until the end of the 2023 financial year and for retaining any profits in order to increase the value of the company through further investments in the market and in new products. A plan regarding the company's dividend policy for the years after 2023 is not yet available. In the case of future, planned distributions to the shareholders of the company, the de facto financial situation may mean that there could be no distribution of dividends to shareholders in these financial years.

Risks related to the company's business model.

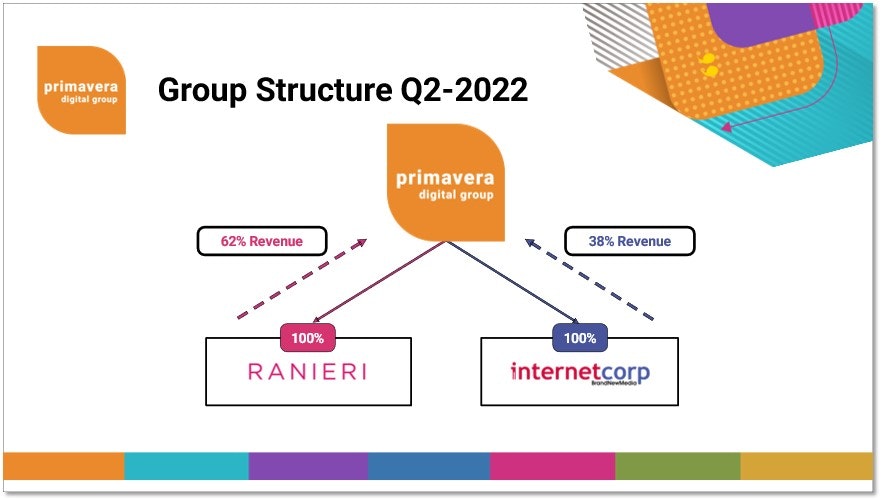

The company is a pure holding company. Revenues of the company are generated exclusively and only on the basis of distributions from the subsidiaries to the issuer. These are provided in the form of turnover-dependent, annual management fees. If a subsidiary shows operating losses or other economic reasons, the issuer may temporarily suspend the collection of management fees. Further revenues may result from interest income from the issuer's internal loans to the subsidiaries.

Risks related to the business model of the Company's subsidiaries.

As a holding company, the issuer is dependent on the business development of its subsidiaries. The business activities of the subsidiaries extend to services in the fields of digital marketing, digital media, public relations and public relations.

Risks due to the pandemic.

So far, the corona pandemic has not noticeably affected the development of the market for advertising and market communication. However, the future impact of the corona pandemic is difficult to assess.

Personnel risks.

There is a risk that Primavera Digital Group Oy will not be able to retain or hire sufficiently qualified employees in the necessary number to implement the business strategy. This applies in particular to employees from the areas of IT (software developer) and online marketing. Due to the loss of employees with corresponding key qualifications, there is a risk that expertise in the developed software and in the field of online marketing or expertise for the further development and maintenance of the software will no longer be available. This could lead, at least temporarily, to difficulties in maintaining the provision of services and the level of performance.

Risks in the development of new software.

When developing new software, misjudgments can occur. In particular, there is a risk that the specified range of functions of the newly developed software does not correspond to the market requirements and/or that the chosen pricing model does not correspond to the prices of competing offers

Risks related to existing and new competitors.

If Primavera Digital Group Oy fails to compete with existing and potential new competitors or to respond to changes in the competitive environment, this may have a negative impact on Primavera Digital Group Oy's revenues, profitability and reduce Primavera Digital Group Oy's customer base.

Risks related to potential litigation.

There are currently no legal proceedings against Primavera Digital Group Oy. However, there is always a risk that Primavera Digital Group Oy will be sued. This could lead to high procedural and legal costs that would adversely affect Primavera Digital Group Oy's financial situation.

RISKS RELATED TO THE MARKET ENVIRONMENT AND REGULATORY FRAMEWORK

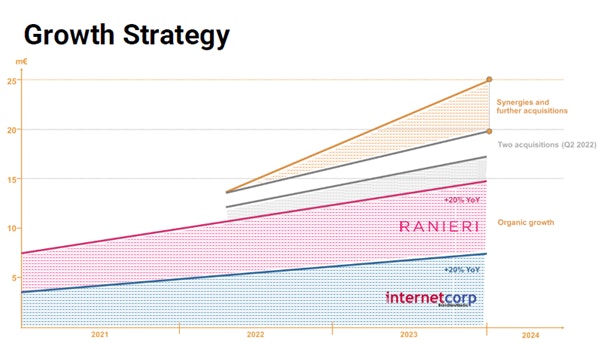

Decisive factors for the economic development of Primavera Digital Group Oy with its business activities just described are the development of the market for advertising and market communication. The market can be negatively affected by rising personnel and purchase prices as well as a weak global economy. Should this market show little or even negative growth, this would lead to cuts in the advertising, marketing and PR budgets of Primavera Digital Group Oy's clients. Macroeconomic changes such as inflation or changes in the regulatory framework can also have a negative impact on the economic development of the issuer and its subsidiaries. Currently, inflation rates in many countries are at record levels, which could lead to an increase in cost pressure and correspondingly to cuts in the advertising, marketing and PR budgets of Primavera Digital Group Oy's customers.

RISK RELATED TO THE POSITION OF THE INVESTOR IN THE EVENT OF INSOLVENCY

Total loss risk.

In the event of insolvency, the shareholders are only satisfied after all creditors have been satisfied from any remaining assets. The shareholders thus bear the full entrepreneurial risk of the company. There is therefore a risk of partial or total loss of the capital invested.

The purchase of the security does not result in any obligation to make additional contributions.

RISK RELATED TO THE FINANCIAL SITUATION OF THE ISSUER

According to the preliminary financial statements for 2021, the issuer has no negative equity.

According to the preliminary annual financial statements for 2021, the issuer has a balance sheet loss of EUR 164,110.80. The annual financial statements prepared for the 2021 financial year have been prepared by the issuer and have not yet been audited.

No insolvency proceedings have been opened against the issuer in the past three years prior to the issue.

The risks listed above are not the only risk factors affecting operations of the company. Also other risks and uncertainty factors that the company currently does not identify or currently considers to be irrelevant may have an integral effect on the business operations, business result, and financial standing of the company.